Spring may be the traditional time of year for cleaning out closets and drawers and organizing attics, but it is also a great time to review of your insurance coverages, according to the Insurance Information Institute.

As your life changes so do your insurance needs. Instead of just dusting around the corners of your insurance policies this year, take the time to read them over and ask yourself the following key questions:

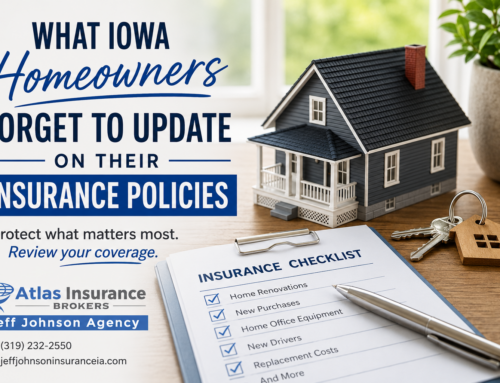

Is my home covered for its full rebuilding cost?

Review your policy to make sure that you have enough insurance to rebuild your home. If you have made major improvements to your home, such as adding a new room, enclosing a porch, or expanding a kitchen or bathroom, you risk being underinsured if you don’t adjust your homeowner’s insurance coverage limits.

And if you don’t yet have a separate flood insurance policy, now would be a great time to check whether your home is in a flood risk zone at FloodSmart.gov.

Do I have enough coverage for expensive items?

Have you bought or received as a gift any valuable jewelry since you purchased/renewed your policy? And when was the last time you had the items, you owned appraised? Standard homeowner’s insurance has dollar limits for the theft of certain types of expensive items like jewelry, furs, and silverware. This means that the insurer will only pay the amount specified in the policy—generally $1,000 to $2,000. To insure these items to their full dollar value, consider a special personal property endorsement or floater. This coverage includes “accidental disappearance,” meaning coverage if you simply lose that item—and there is no deductible.

But remember that items can go up or down in value. Floaters and endorsements are priced on the appraised value of an item or collection so have periodic reappraisals done to make sure you are purchasing only the amount of coverage you need.

The best way to keep track of your belongings and make sure they are adequately insured is to create a home inventory—find out how here

Do I still need comprehensive/collision on my car?

As your cars get older and become worthless and less, you may want to consider saving insurance premiums by dropping comprehensive and/or collision coverages and carrying liability-only insurance. You essentially would be “self-insuring” your vehicle and would be responsible for repairing or replacing your vehicle if you were in an accident and had a claim. Jeff or Dan can run the cost and premium scenarios for you and answer any questions to help you make an informed decision.

Do I have enough liability insurance to fully protect my assets?

Standard homeowners and auto policies liability coverage, paying for judgments against you and your legal fees, up to a limit set in the policy. However, in our litigious society, you may want to have additional protection—that is what an umbrella liability policy provides. An umbrella policy kicks in when you reach the limit on the underlying liability coverage in homeowners, renters, condo, or auto policy. If your assets have increased of late, you’ll have more to lose and may want to consider this extra layer of protection.

What kind of vacation will I be taking this summer?

If you are taking an expensive, pre-paid vacation or an active vacation such as biking or hiking in an exotic locale, travel insurance can help protect the financial investment in your vacation.

Most importantly, whether it’s winter, spring, summer, or fall, plan a regular talk with Jeff or Dan at Jeff Johnson Insurance Agency to ensure you get the appropriate coverages for all of your insurance needs.